All Categories

Featured

Table of Contents

For many people, the biggest problem with the unlimited financial idea is that first hit to very early liquidity triggered by the prices. This disadvantage of limitless banking can be minimized significantly with correct policy design, the initial years will constantly be the worst years with any kind of Whole Life plan.

That said, there are certain unlimited financial life insurance policy policies developed mostly for high early cash money worth (HECV) of over 90% in the first year. Nevertheless, the lasting efficiency will certainly frequently substantially lag the best-performing Infinite Banking life insurance policy policies. Having accessibility to that extra four figures in the first couple of years might come with the cost of 6-figures in the future.

You really get some substantial lasting advantages that aid you recoup these early prices and after that some. We discover that this impeded early liquidity trouble with boundless banking is extra psychological than anything else once extensively discovered. Actually, if they absolutely needed every cent of the money missing from their infinite financial life insurance policy policy in the first couple of years.

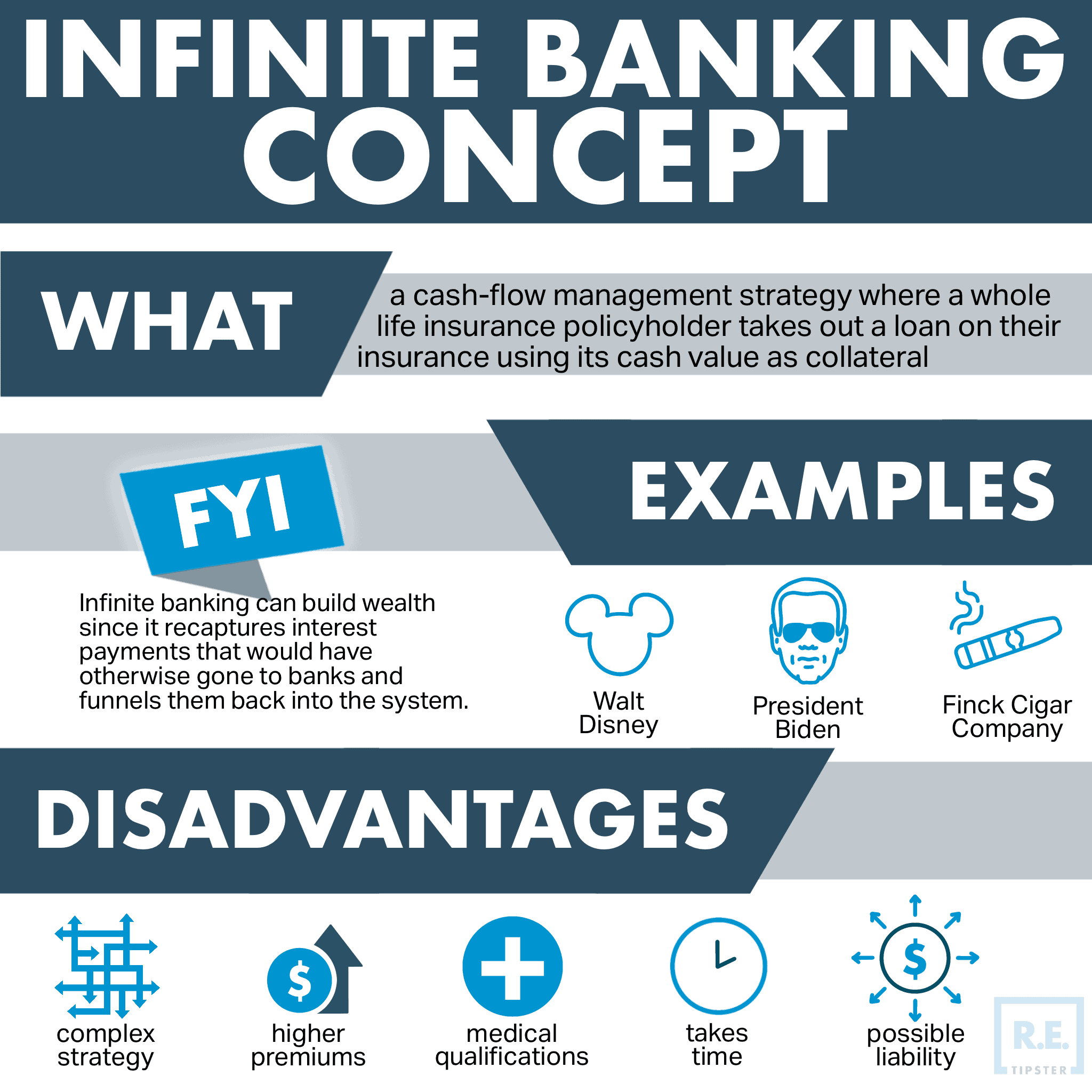

Tag: infinite banking concept In this episode, I speak about funds with Mary Jo Irmen that shows the Infinite Banking Concept. This topic might be debatable, however I desire to obtain diverse views on the program and discover about various approaches for farm financial management. Several of you might concur and others will not, yet Mary Jo brings a really... With the increase of TikTok as an information-sharing system, economic advice and approaches have discovered a novel means of dispersing. One such strategy that has been making the rounds is the boundless financial idea, or IBC for short, gathering endorsements from stars like rapper Waka Flocka Flame. While the approach is currently prominent, its origins trace back to the 1980s when financial expert Nelson Nash presented it to the world.

Within these plans, the cash worth grows based upon a rate established by the insurance provider. Once a considerable cash value collects, insurance holders can obtain a money value lending. These finances differ from standard ones, with life insurance policy working as collateral, indicating one might shed their protection if borrowing excessively without appropriate cash money worth to support the insurance coverage prices.

And while the allure of these plans is evident, there are innate limitations and risks, necessitating persistent money value monitoring. The technique's authenticity isn't black and white. For high-net-worth people or service owners, especially those making use of methods like company-owned life insurance policy (COLI), the benefits of tax breaks and substance growth might be appealing.

Infinity Banca

The appeal of boundless banking doesn't negate its challenges: Price: The foundational need, a permanent life insurance policy plan, is more expensive than its term equivalents. Qualification: Not everybody receives whole life insurance policy as a result of strenuous underwriting processes that can leave out those with specific health and wellness or way of living problems. Intricacy and risk: The intricate nature of IBC, paired with its dangers, may deter many, specifically when easier and much less risky choices are offered.

Designating around 10% of your monthly earnings to the policy is just not possible for most people. Part of what you check out below is merely a reiteration of what has currently been said over.

Before you get yourself right into a scenario you're not prepared for, understand the complying with initially: Although the concept is typically marketed as such, you're not in fact taking a funding from yourself. If that were the instance, you wouldn't have to repay it. Instead, you're borrowing from the insurance coverage business and have to settle it with interest.

Some social networks blog posts suggest using cash money worth from whole life insurance policy to pay down bank card financial debt. The idea is that when you pay off the car loan with passion, the quantity will be sent out back to your investments. Unfortunately, that's not how it functions. When you repay the loan, a section of that passion mosts likely to the insurer.

For the first several years, you'll be repaying the payment. This makes it exceptionally challenging for your policy to collect worth during this time around. Entire life insurance coverage expenses 5 to 15 times more than term insurance coverage. Many people just can not manage it. Unless you can manage to pay a few to a number of hundred bucks for the following decade or more, IBC won't work for you.

Infinite Bank Statements

If you call for life insurance coverage, right here are some useful suggestions to think about: Think about term life insurance coverage. Make certain to shop about for the ideal price.

Copyright (c) 2023, Intercom, Inc. () with Scheduled Typeface Name "Montserrat". Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Scheduled Font Style Call "Montserrat".

Bank On Yourself Complaints

As a certified public accountant specializing in actual estate investing, I have actually brushed shoulders with the "Infinite Banking Principle" (IBC) extra times than I can count. I have actually even talked to experts on the topic. The primary draw, in addition to the noticeable life insurance policy advantages, was constantly the idea of building up cash money value within a permanent life insurance policy policy and loaning versus it.

Certain, that makes good sense. But truthfully, I constantly assumed that cash would be better invested directly on financial investments rather than funneling it through a life insurance policy policy Up until I found exactly how IBC might be integrated with an Irrevocable Life Insurance Depend On (ILIT) to create generational wide range. Allow's begin with the essentials.

Infinite Banking Concept Pdf

When you borrow versus your plan's cash money worth, there's no collection repayment timetable, offering you the flexibility to manage the car loan on your terms. Meanwhile, the cash value proceeds to expand based on the plan's assurances and dividends. This setup enables you to access liquidity without interrupting the long-lasting growth of your policy, offered that the lending and interest are taken care of wisely.

The process proceeds with future generations. As grandchildren are birthed and grow up, the ILIT can acquire life insurance policy plans on their lives. The trust after that collects several policies, each with expanding cash money worths and death advantages. With these policies in place, the ILIT properly ends up being a "Family members Bank." Family members can take finances from the ILIT, using the cash money value of the policies to money financial investments, start companies, or cover major expenditures.

A crucial aspect of managing this Household Bank is making use of the HEMS criterion, which means "Health and wellness, Education, Maintenance, or Support." This standard is usually included in count on agreements to direct the trustee on just how they can distribute funds to beneficiaries. By adhering to the HEMS requirement, the count on makes sure that distributions are created vital needs and long-term support, safeguarding the trust's assets while still offering relative.

Boosted Flexibility: Unlike rigid bank fundings, you control the payment terms when obtaining from your very own policy. This enables you to framework payments in such a way that lines up with your service capital. infinite banking concept canada. Better Cash Circulation: By financing service expenditures through policy loans, you can potentially maximize money that would otherwise be bound in standard funding payments or equipment leases

He has the same devices, however has actually also constructed added money value in his policy and received tax advantages. Plus, he now has $50,000 readily available in his plan to utilize for future chances or expenditures. Regardless of its possible advantages, some people stay hesitant of the Infinite Financial Idea. Let's address a few usual concerns: "Isn't this simply pricey life insurance policy?" While it holds true that the premiums for an effectively structured entire life policy might be greater than term insurance policy, it is very important to see it as more than simply life insurance policy.

Infinite Banking Concept Spreadsheet

It's regarding developing a versatile financing system that gives you control and supplies several advantages. When used purposefully, it can complement various other financial investments and service strategies. If you're interested by the possibility of the Infinite Banking Principle for your company, right here are some steps to take into consideration: Educate Yourself: Dive much deeper right into the principle via respectable books, seminars, or consultations with knowledgeable professionals.

{kind=link}

Latest Posts

Unlocking Wealth: Can You Use Life Insurance As A Bank?

Infinite Insurance And Financial Services

Becoming Your Own Banker Nash