All Categories

Featured

Table of Contents

[/image][=video]

[/video]

Holding cash in an IUL fixed account being credited interest can typically be far better than holding the cash money on deposit at a bank.: You've constantly desired for opening your very own bakeshop. You can borrow from your IUL policy to cover the initial expenditures of leasing a space, buying equipment, and employing team.

Personal fundings can be gotten from typical financial institutions and credit report unions. Below are some crucial points to think about. Charge card can give a flexible means to obtain money for very temporary durations. Borrowing cash on a debt card is generally really pricey with annual portion rates of interest (APR) typically getting to 20% to 30% or even more a year.

The tax therapy of policy car loans can vary considerably relying on your nation of home and the specific regards to your IUL plan. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, policy lendings are normally tax-free, supplying a substantial advantage. However, in other jurisdictions, there might be tax effects to consider, such as possible taxes on the loan.

Term life insurance policy just provides a fatality advantage, without any kind of cash worth build-up. This suggests there's no cash money worth to obtain versus.

R Nelson Nash Net Worth

Picture entering the monetary universe where you're the master of your domain name, crafting your very own course with the finesse of a skilled banker but without the constraints of towering institutions. Invite to the globe of Infinite Financial, where your financial fate is not simply an opportunity but a tangible fact.

Uncategorized Feb 25, 2025 Cash is just one of those things most of us manage, but a lot of us were never truly educated how to utilize it to our advantage. We're informed to save, spend, and budget, however the system we operate in is made to keep us based on financial institutions, frequently paying interest and costs simply to access our very own cash.

She's a professional in Infinite Financial, a technique that assists you take back control of your funds and construct actual, lasting wealth. And trust methis isn't some "finance brother" magic technique. It's an actual technique that rich families like the Rockefellers and Rothschilds have actually been utilizing for generations. Let's obtain into it.

Now, before you roll your eyes and assume, Wait, life insurance policy? This is a high-cash-value policy that allows you to: Shop your cash in a place where it grows tax-free Borrow against it whenever you need to make financial investments or significant acquisitions Make nonstop substance passion on your money, even when you obtain versus it Think about just how a financial institution works.

With Infinite Financial, you come to be the bank, making that passion rather of paying it. For many of us, cash streams out of our hands the second we get it.

How To Train Yourself To Financial Freedom In 5 Steps

The insurance provider does not require to obtain "paid back," because it will certainly just be subtracted from what gets distributed to your beneficiaries upon your expiration date, as Hannah so euphemistically called it. You pay yourself back with rate of interest, similar to a financial institution wouldbut currently, you're the one making money. Let that sink in.

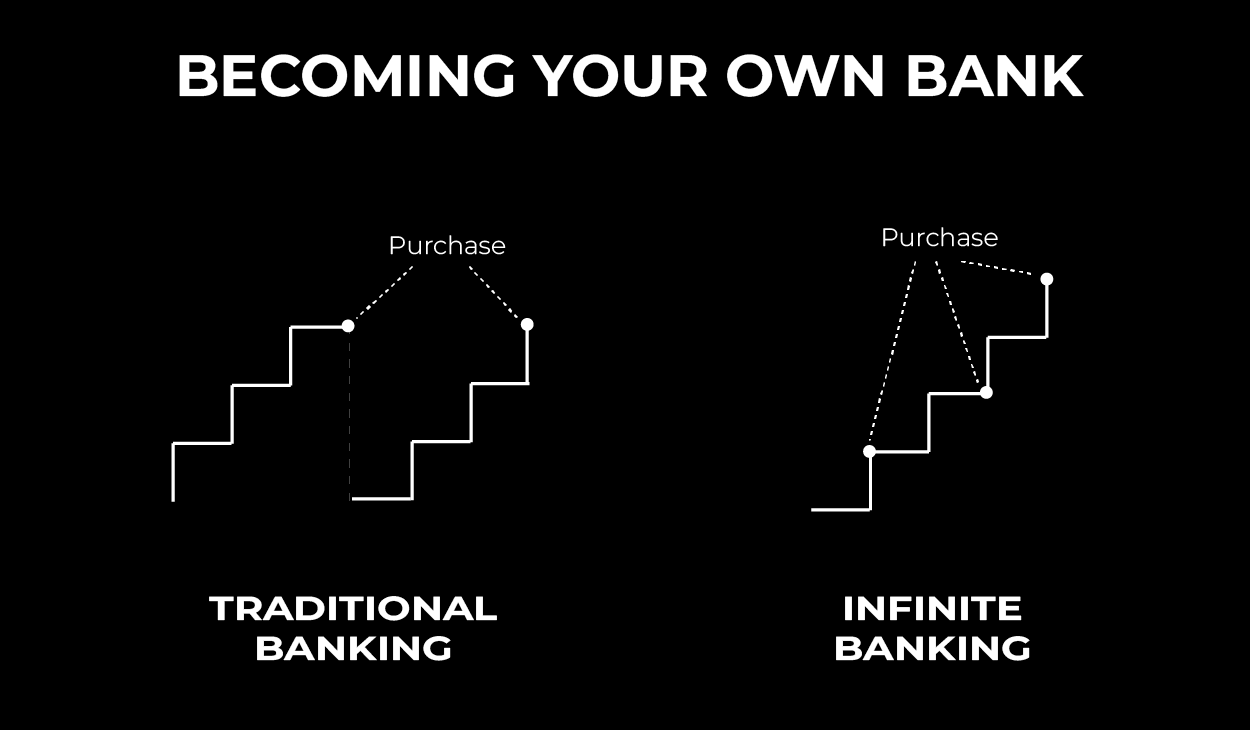

It's regarding redirecting your money in a means that develops wide range instead of draining it. Instead of going to a bank for a car loan, you obtain from your very own plan for the down payment.

You utilize the financing to purchase your residential or commercial property. Rental earnings or benefit from the offer repay your policy rather than a bank. This indicates you're constructing equity in your plan AND in realty at the very same time. That's what Hannah calls double-dippingand it's exactly how the well-off keep expanding their money.

Start Your Own Personal Bank

Right here's the thingthis isn't a financial investment; it's a cost savings method. Your cash is assured to expand no matter what the supply market is doing. You can still invest in genuine estate, supplies, or businessesbut you run your cash via your policy first, so it maintains growing while you invest.

We've been trained to assume that banks hold the power, yet the truth isyou can take that power back. Hannah's household has been utilizing this method considering that 2008, and they now have over 38 plans moneying actual estate, investments, and their family's financial legacy.

Becoming Your Own Lender is a text for a ten-hour course of instruction regarding the power of dividend-paying entire life insurance policy. It is not a sales device permanently insurance representatives. It is education and learning that the life insurance policy sector must have instructed during the last 200 years. The market has concentrated on the death advantage top qualities of the agreement and has neglected to properly describe the funding capacities that it offers for the policy proprietors.

This book shows that your need for finance, during your life time, is a lot more than your demand for protection. Solve for this demand via this instrument and you will wind up with even more life insurance coverage than the business will certainly provide on you. The majority of every person is familiar with the fact that can borrow from an entire life plan, however as a result of exactly how little costs they pay, there is restricted access to money to fund major things required throughout a lifetime.

Really, all this publication includes in the formula is scale.

{kind=link}

Latest Posts

Unlocking Wealth: Can You Use Life Insurance As A Bank?

Infinite Insurance And Financial Services

Becoming Your Own Banker Nash